The Best Fluffy Pancakes recipe you will fall in love with. Full of tips and tricks to help you make the best pancakes.

People define health across many life-flows: physical health, mental health, social health, appearance (“how I look impacts how I feel”) and, to be sure, financial well-being.

In tracking this last health factor for U.S. consumers, several pollsters are painting a picture of financially-stressed Americans as President Trump tallies his first six weeks into the job. The top-line of the studies is that the percent of people in America feeling financially wobbly has increased since the fourth quarter of 2024. I’ll review these studies in this post, and discuss several potential impacts we should keep in mind for peoples’ health and care in 2025 and beyond. You’ll read updates from Ipsos, West Health-Gallup, the University of Michigan, and finally the wonky (but very informative) Fed Beige Book from the Federal Reserve.

![]()

Start with the Ipsos Consumer Tracker for February 2025, which identified a rise in U.S. consumers feeling less comfortable about their economic status now compared with mid-November 2024. The erosion in household fiscal comfort fell across income categories, with a significant 21-point drop in families earning at least $100,000 a year. ![]()

The largest fall in financial wellness perceptions happened among folks over age 55, posting the biggest drop of 23 percentage points. (More on this voting-apt population in the Hot Points, below).

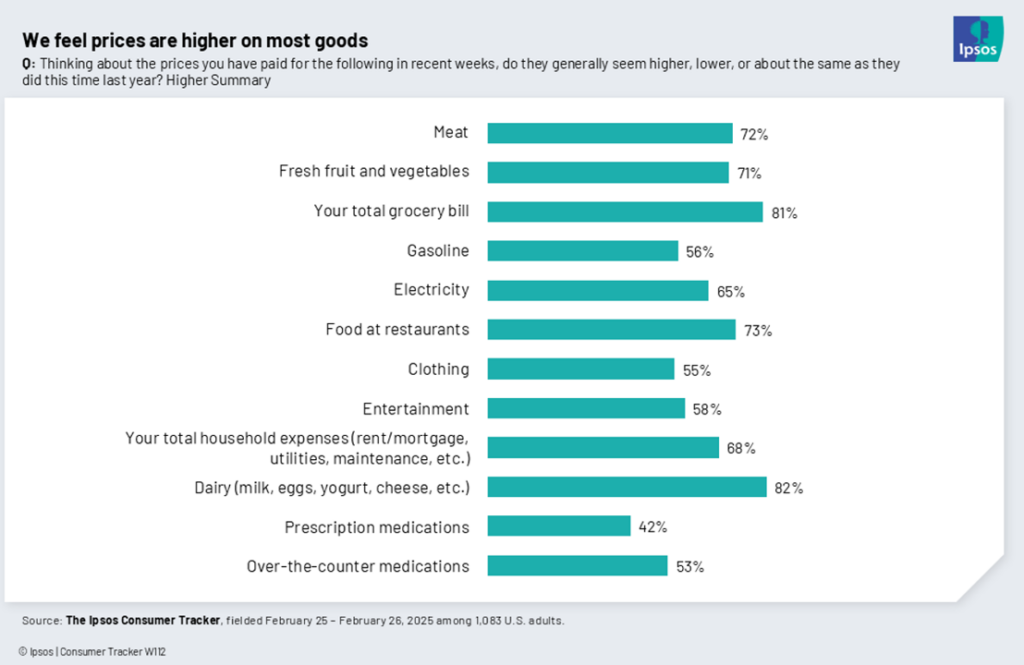

“It’s not just eggs,” Ipsos says: U.S. consumers feel most costs of living are up in the first quarter of 2025. Note that 52% of consumers said their over-the-counter medication prices seemed higher this year, and 42% called out prescription meds being more expensive.

Two-thirds of people said their total household expenses (rent/mortgage, utilities, maintenance) were higher this year than last.

Specific to consumers home health care economics, we learn from Gallup and West Health that Americans borrowed about $74 billion to pay medical bills in 2024. That’s about 30 million U.S. consumers who borrowed money to pay for health care in the past year.

These two graphs from Gallup-West Health’s survey tell us that even the most affluent households earning at least $180,000 a year are concerned about medical debt — that’s 40% of these top-income consumers. Furthermore, see that the median amount borrowed for health care triples among people 50 years of age and older.

And women are more likely than men in America to have to borrow money to pay for care for themselves or a member of their household, the study discovered.

With the data from Ipsos, Gallup and West Health in the plotline, we now turn to the monthly Consumer Sentiment Index from my alma mater, the University of Michigan, which shows us that sentiment in February 2025 fell to a low level last seen in summer 2024. A year ago in February 2024, the CSI was 76.9.; the current index fell to 65.7.

U.S. consumers have grown uneasy about many factors that shape both the macro and their household economics, with over half of people expecting unemployment to rise in the next year — the highest share since the pandemic recession. Joanne Hsu, director of the University of Michigan’s Surveys of Consumers, commented,

“Consumers’ expectations for the path of inflation worsened considerably this month; they are clearly bracing for a resurgence in inflation. …Consumers broadly anticipate that tariff hikes will lead to higher inflation.”

Now, on to the Federal Reserve’s Beige Book. The Fed publishes this report eight times a year based on input from the 12 Federal Reserve Districts in the U.S. (Atlanta, Boston, Chicago, Cleveland, Dallas, Kansas City, Minneapolis, New York, Philadelphia, Richmond, San Francisco, and St. Louis), based on regional economic activity – describing conditions for labor markets, prices, business and economic activity.

The key finding for us to focus on in this big book is economic activity among consumers: the Fed notes right up front in the National Summary, “Consumer spending was lower on balance, with reports of solid demand for essential goods mixed with increased price sensitivity for discretionary items, particularly among lower-income shoppers…..Vehicle sales were modestly lower on balance.”

Here’s more on the Beige Book…

Health Populi’s Hot Points: We can be certain that the economic state of mind for U.S. health consumers is on the downturn across economic categories.

We then ask the question, how will Americans’ perceptions of financial un-wellness impact their health care and health behaviors? I’ll point to 3 very current situations with uncertainties and huge import: medical bills and the shuttering of the Consumer Financial Protection Bureau (CFPB), Medicaid as a health insurance plan, and Social Security as a promised safety net program for aging Americans.

We can start with the consumer as patient and medical bill payor, noting that even the most affluent households in the Gallup-West Health study feel the sting of medical bill concerns. On that point, the recent shutdown of the Consumer Financial Protection Bureau has implications for medical bills and Americans’ credit scores. More broadly if the CFPB ultimately disappears as an agency (currently on-hold via a court order), more macro consumer woes such as credit card and bank fees could go unregulated to the extent that CFPB improved American consumers’ financial wellbeing such as removing medical bills from credit reports (e.g., FICO scores).

Next, consider a quite-possible America where Medicaid erodes for some of the most vulnerable people in the nation. Medicaid pays for 40% of the births in the U.S. (and 50% of births in rural communities), long-term care for millions of people, and a safety net for people who need emergency and urgent care, among other roles for keeping people healthy and productive at their workplaces which includes the heavy lift of home-caregiving and caring. There is noise and uncertainty about how Medicaid will be managed in President Trump’s administration, as well as how a GOP-led Congress will deal with the health plan in a new budget design and also how Elon Musk’s DOGE team could define “fraud and abuse” in the program. A wild card here are the 50 State Governors, where even a handful of Republican state leaders have expanded Medicaid and value doing so for their resident health citizens.

In addition to uncertainties about Medicaid’s status, the Congressional Budget Office (CBO) issued a report this week that calculates the Federal budget cut of $))) in the currently discussed GOP-led plan would require cuts to both Medicaid and could also impact Medicare. The specific language can be found in this letter from CBO to House of Representatives Ranking Members Boyle and Ranking Member Pallone.

Next, consider the aging of America and the nation’s promise, since President Roosevelt’s leadership, of the Social Security program.

Among the most avid voters in the U.S. are older people. The AARP gives us a view into what older people might be thinking right now in this snippet from an email I received this week on March 3, 2025 (as a paying member of AARP).

The call-out by DOGE-head Elon Musk that “Social Security is a Ponzi scheme” made some seniors’ heads go on fire and was a definitely signal that AARP is raising. Another Ipsos poll found that older U.S. consumers are very concerned about the cost of food and consumers goods. Combined with potential changes (downward) to Social Security payments and Medicare coverage will be on older peoples’ minds and pressured pocketbooks for the coming months as U.S. health citizens gain greater clarity and insights into these much-beloved public policies.

Ipsos writes,

Given that older Americans are more likely to own stocks, they may feel more vulnerable to market volatility and all-around economic uncertainty. And that’s not to mention the fear of threats to Medicare and Social Security. But it’s not just about big-picture worst-case scenarios. Older Americans (i.e. retirees) are more likely to rely on fixed incomes which could encourage them to pay closer attention to their budgets. Americans earlier in their lives and careers might toss their receipts sight unseen.”

There are many factors and moving parts shaking up the tectonic forces of health care in the U.S. as I finish up this post. Uncertainties and grey areas prevail, with very shaky financial markets domestically and globally — all impacting various segments of health care systems — from hospitals and health plans to pharmaceuticals and medical devices, clinical labor markets and researchers (namely – might the U.S. experience a “brain drain” of brilliant researchers to, say Ireland and the Netherlands?)….and what of innovation in digital health and telehealth?

These are issues that I’m addressing in my advisory work “right now,” which I wished to share with you in the moment. We will keep tracking these issues very closely, hoping for the best for all U.S. health citizens and, truly, for public health and health citizenship around the world.